|

|

| Creditors and a List of Former Attempted Buyers of SCO Get a Notice of the Auction - Updated 6Xs |

|

|

Friday, September 17 2010 @ 03:59 PM EDT

|

There is a humungous filling in the SCO bankruptcy, 184 pages, showing all the recipients who were sent the order [PDF] by the court authorizing the auction of substantially all of SCO's assets. Of course, they have to give notice to everyone who might be affected, all the creditors, 8,302 in all. Poor things. What will they ever get from SCO? A plugged nickel, maybe. But that's not the interesting part. Look at the last page of the PDF. It seems to be a list of former attempted buyers, and maybe it's a list of the potential buyers once again. Of course, Steve Norris and the unXis gang is on the list. So are some others that have tried to buy assets from SCO before, like York. I'll show you the entire list.

Here's the 184-page filing:

09/16/2010 - 1171 - Affidavit/Declaration of Service of Konstantina Haidopoulos (related document(s) 1161 ) Filed by Edward N. Cahn, Chapter 11 Trustee for The SCO Group, Inc., et al.. (Fatell, Bonnie) (Entered: 09/16/2010)

And here's the list, which is given no title or header, which is why we can only guess, minus the addresses, because I'm nicer than SCOfolk:

Riptide (formerly Shea Development Corp)

LNS Acquisition LLC

Attention: Charles C. Hale

JGD Management Corp. d/b/a York Capital Management

Platinum Equity

Versata, Inc.

LSC Holdings LLC

unXis, Inc.

c/o MerchantBridge & Co, Ltd.

Attention: Eric Le Blan

We've seen all of them before. Here's Platinum Equity, in Darl McBride's mouth at the bankruptcy hearing in June of 2009, the famous one where the judge asked what would happen to him if he didn't meet a deadline, take him out back and shoot him? Sigh. You'll find LSC Holdings mentioned also on that page. Of course you remember unXis and the York-Hale-LSN connections. [ Update: Wow. There's a connection between Platinum Equity and Ocean Park Advisors, who arranged the auction for the SCO Group. Here is their bio for Mark Comer: Mr. Comer is the founder and a Managing Director of Ocean Park Advisors. He has decades of experience in business development, finance and operations both in the US and Asia. He has advised boards, funds, owners and lenders on growth strategies, capital structures, acquisitions, divestitures, restructurings and operational issues. Prior to founding Ocean Park, he was a Principal and SVP at Platinum Equity, where he played a key role in raising the firm’s $700 million first-time fund and was active in managing the firm’s $4 billion revenue portfolio. Are we in the Ozarks or something, where everyone is creepily related to everyone else, and deeper, is Ocean Park a neutral party? Lordy, what a picture.] The only one that was not fully out in the light is Shea Development Corp, now calling itself Riptide, but they've been in the shadows from way back. I did some research on them long ago, but then the proposed deal didn't happen, and I never published it. The overview: look at the management of these two entities.

Frank Wilde was CEO of Shea, which bought Riptide in 2007. Here's Riptide's most recent SEC filing, apparently the last one, back in 2009, and

the most recent 10Q. Lots of litigation. Most of their revenues from the US Army.

Shea's old SEC filings are in there also, and you can find them by searching for Riptide. Here's the link that matters, because it ties it all up with a bow: the 8K showing the link to Renaissance Capital: On May 18, 2007, representatives of Shea Development Corp. (the “Company”) began making presentations at the RENN Investor Conference in Dallas, Texas, hosted by Renaissance Capital Growth & Income Fund III, Inc. using slides containing the information attached to this Current Report on Form 8-K as Exhibit 99.1.

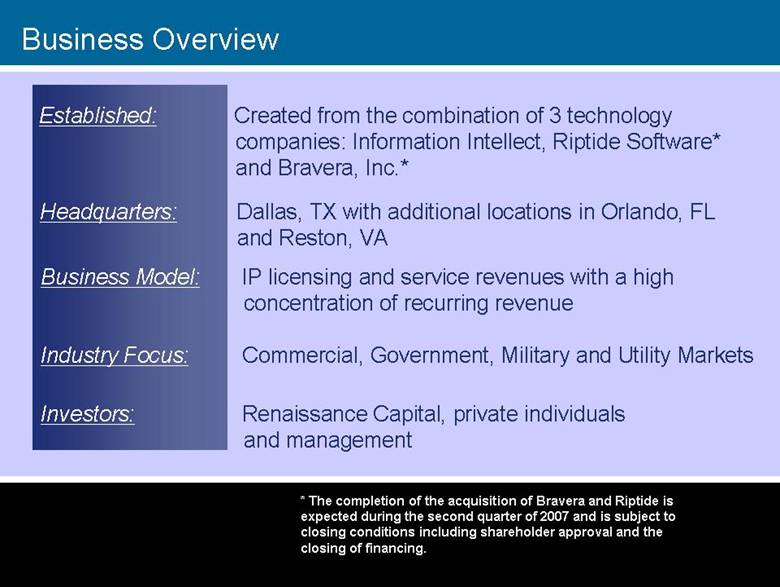

And here are all the graphics from that presentation in 2007. Here's the one showing that Renaissance Capital was one of the investors in Shea, along with management and private investors. And the business model, it says, is "IP licensing and service revenues with a high concentration of recurring revenue." Like what? SCOsource, maybe? [ Update 2: How would Renaissance Capital get interested in SCO? Well, take a look at

this SEC filing for CaminoSoft Corp., which informs us that Robert Pearson "who became a director in 1997, has been

associated with Renaissance Capital Group ("RCG") since April 1994." Others listed as shareholders of RENN Capital Group are Russell Cleveland and John Schmidt. And a Michael Skelton is listed as joining as CEO and director of CaminoSoft in 2004, and his bio tells us he was, from 1993 to 1995, "Vice President of Sales and Marketing for SCO Inc., a

company that provides UNIX operating system software." So maybe that's how. What does that have to do with Shea, though, you ask? In 2007, CaminoSoft and Shea proposed merging together. Here's the S4 filed with the SEC about it, and in the list of the execs we find that "RCG is the investment advisor of the largest shareholders of CaminoSoft." However in 2008, CaminoSoft terminated the merger agreement with Riptide.]

Shea's customers.

Another one with more detail. And this graphic indicates that Riptide is now a private company.

The

management team, ladies and gentlemen. Do you see the TTLA in the bio section for Frank Wilde? Yes, that stands for Tarantella, formerly known as the Santa Cruz Operation. Joseph Vitetta, also formerly with Tarantella, is also on that management list. And in 2007, guess who else joined the Shea board? Alok Mohan. Would that not be our old friend Alok Mohan, the ex-CEO of Santa Cruz, who swore up and down at the SCO v. Novell trial, via his video deposition, that he thought SCO got the copyrights in 1995? Why, yes. The very same. Any advantage to him and Shea or now Riptide if that testimony had prevailed? Perhaps I should say SCO's old friend. Get the picture?

If not, take a look at this last slide, the company strategy, which it says was to "extend the reach of Microsoft products". Yessir, the gang's all here, hovering like vultures on low-hanging branches just waiting by the roadside as the SCO funeral procession begins its march.

Update 6: That's when Wilde climbed on board Tarantella also, according to this Tarantella 10K for the fiscal year ended September 30, 2004, and by then Tarantella was not doing well either:

On December 11, 2003, we announced that our board of directors had appointed Francis E. Wilde as Chief Executive Officer (CEO), President and a member of our board of directors. Mr. Wilde succeeds Douglas Michels, who continues with us as a strategic advisor to Tarantella, focusing initially on merger and acquisition opportunities. Mr. Michels will also continue as a director of Tarantella.

In December 2003, Gregory Quinn and E. Joseph Vitetta, Jr. joined us as our Vice President North American Operations and Strategic Alliances and Vice President Corporate Development, respectively. In January 2004, Mr. Vitetta was also appointed Corporate Secretary, and in October 2004, also assumed the role of Managing Director of EMEA. Stephen Bannerman joined us in December 2003 as Vice President Corporate Marketing, and his title was subsequently changed to Chief Marketing Officer. Joseph Makoid joined us in January 2004 as our Vice President OEM Sales. Messrs. Quinn, Bannerman, Vitetta and Makoid all report directly to Mr. Wilde. On January 6, 2004, we announced the appointment of John M. Greeley as Chief Financial Officer (CFO), reporting directly to Mr. Wilde. Mr. Greeley assumed the CFO responsibilities from Mr. Alok Mohan, who had been serving as acting CFO since September 8, 2003….

We divested our server software and professional services divisions in May 2001. Since the divestiture, we have not achieved profitability, and may never generate sufficient revenues to achieve profitability. As of September 30, 2004 we had an accumulated deficit of $140.5 million. …

Our corporate actions are substantially controlled by principal shareholders.

Our principal shareholders beneficially own approximately 51% of our outstanding common stock. These shareholders, if they acted together, could exert substantial control over matters requiring approval by our shareholders, including electing directors and approving mergers or other business combination transactions. This concentration of ownership may also influence the outcome of a change in control of our company, which could deprive our shareholders of an opportunity to receive a premium for their stock as part of a sale of our company and might reduce our stock price. These actions may be taken even if they are opposed by our other shareholders....

Mohan was Chairman at that time and had been since 1998. He had been President and CEO already since 1994 and 1995 respectively and elected to the board in 1994. In 1999, the 10K continues, Mohan entered into a consulting agreement with the company for which he was paid $126,000 per year. In 2000, that was altered to $5,000 a month, to last until the completion of the acquisition by Caldera of the two Santa Cruz, now Tarantella, business units, and then it was extended through 2004 at $180,000 a year, with incentive payments according to the terms of the company's incentive plan. Then in 2004, he got a new agreement, paid $22,500 a year plus 67,500 shares of restricted stock, and target incentives of $90,000. The following year was similar, plus health benefits. For participation on the board, he got $25,000 annually, 25% in cash and the rest in stock. Others started to take stock grants also in 2003:Restricted stock grants from December 2003

In December 2003, we entered into an agreement with five of our senior executives and directors under which the senior executives and directors received restricted common stock in lieu of salary for portions of their calendar year 2004 compensation. The shares are valued at $0.93 per share, which was the fair market value of the shares at the time of the agreement. A total of 570,250 shares were issued to the following individuals:

-

Francis E. Wilde 50,000 shares

- Ron Lachman 18,750 shares

- Randy Bresee 105,000 shares

- Alok Mohan 68,000 shares

- Douglas Michels 328,500 shares

By this point, Doug Michels is no longer the CEO, being now a "strategic advisor".

Update 3: I forgot Versata. Here's the article from 2007 where you can find Versata listed in a Mesirow bill. On Exhibit D-9, you find these entries:

| Name |

Date |

Description |

Time |

Rate |

Amount |

| Feltman, James |

10/04/07 |

Perform analysis of Versata and York proposals. |

1.1 |

690.00 |

759.00 |

| Fasel, Bill |

10/25/07 |

Participate in conference call with S. Fallon (Versata Enterprises) and T. Zoha (MFC) to provide an update of the Sale Process, Bid Procedures Motion and next steps. |

0.8 |

650.00 |

520.00 |

There are others. And here are Mssrs. Wilde and Vitetta:

| Name |

Date |

Description |

Time |

Rate |

Amount |

| Fasel, Bill |

10/12/07 |

Participate in conference call with F. Wilde (Chairman and CEO) and J. Vitteta (Senior Vice President, Corporate Secretary) of Bidder 2 and T. Zoha, S. Smith and C. McClellan (all MFC) to discuss Bidder 2 term sheet for SCO's UN business. |

0.7 |

650.00 |

455.00 |

| McClellan, Christian |

10/01/07 |

Participate in conference call with F. Wilde (Chairman and CEO) and 1. Vitteta (Senior Vice President, Corporate Secretary) of Bidder 2 and B. Fasel, S. Smith and T. Zoha (all MFC) to discuss Bidder 2 term sheet for SCO's UN business. |

0.7 |

240.00 |

168.00 |

Update 5:

Here's an interview by Matt Cooper of WallSt.net, attached as an exhibit to an 8K back on November 6, 2007, with the then President of Shea Development Corporation, Philip Loeffel, as he describes Shea's software business:Phil: Very good. Shea Development is a growing technology company that’s strategically acquiring other profitable technology companies. Through its subsidiary, MeterMesh, Shea provides state of the art advanced metering infrastructure technology to small and midsized utilities. Bravera, also a subsidiary, provides business process management and work flow automation primarily to government agencies. Riptide Software, a leader in considerable enterprises class software, is the largest subsidiary of Shea and provides a strong foundation for growth.

Matt: Great.

Phil: Our company delivers our customers process management software solutions and service offerings that improve their customer’s ability to manage critical business processes, improve efficiency and provide world class customer service. These enterprise wide software solutions use the latest technology including on demand capabilities, mobility platforms, and real time data access to empower businesses to make better decisions for their customers. The efficiencies gained through automation of key business processes improve our customer’s bottom line often allowing our software solutions to pay for themselves over a very short period.

Our software library has been strategically developed for reusability to provide rapid development of new products which support emerging needs of a new customers. Literally millions of lines of software which support numerous enterprise systems in use today were developed over the last ten years. With a software library that focuses on reusable components to supports enterprise level software solutions, we’ve captured significant market share in the aerospace, customer relationship management, modeling and simulation and distant learning application space. Recent merger and acquisition activity has provided the opportunity to leverage this software library into several new vertical markets, greatly reducing our over all time to market for new product offerings. Our ability to provide low cost enterprise level software solutions to a wider variety of customers has been enhanced through our recent consolidation efforts which strategically combine key technology components eliminating the need for long development cycles. These combinations have allowed the company’s offerings to expand well beyond our vertical focus which has positioned our company for significant growth in the coming year.

It sounds like the company was just swimming along, but here's a Notification of Late Filing, dated March 31, 2008, asking the SEC for an extension of time to file their 10K, and here's how it really turned out:The Company expects to report revenue of approximately $7.2 million, a loss from continuing operations of approximately $19.9 million and a loss applicable to common shareholders of approximately $20.4 million. These amounts are pending the completion of the audit and are subject to change. The extension to April 15, 2008 will provide the Company enough time to complete and file Form 10-KSB. In April, they

filed a 10KSB, with the header Annual and Transition Reports of Small Business Issuers, and that's how we find out that Shea changed its name to Riptide in January of 2008 and we also find out how they were actually doing:Effective January 2, 2008, the Registrant, formerly known as Shea Development Corp., changed its name to Riptide Worldwide Inc. (“Riptide,” the “Company” or the “Registrant”) and trades on the OTCBB under the symbol “RTWW”. Riptide was incorporated in the state of Nevada on February 18, 2005 and acquired Information Intellect, Inc. (“Information Intellect”) on March 2, 2007 in a transaction accounted for as a reverse merger. Prior to March 2, 2007, Riptide was a shell company and had minimal business activities which were unrelated to its current business activities. Since the merger on March 2, 2007, Riptide has expanded its products and is transitioning its business into a business process management (BPM) and information technology services company. Riptide has continued this transition through strategic acquisitions and in July, 2007, Riptide completed the acquisition of Riptide Software, Inc.(“Riptide Software”) and Bravera, Inc. Riptide Software provides custom programming services to build configurable enterprise software solutions for revenue and financial management systems, enterprise application integration, user-interface frameworks, middle-tier frameworks, military and commercial modeling and simulation, and military C3 Centers (Command, Control and Communications). Riptide Software’s enterprise software products provide customers with a wide array of options to make the product their own through a customizable configuration process. On January 30, 2008, Bravera, Inc. changed its name to RTWW Business Services Inc. (“RBS”) and provides outsourced business services to customers including document scanning and management services. These services are offered to agencies of the federal government including FEMA, (the Federal Emergency Management Agency), as well as commercial customers. The Company continued to execute its strategy of growth through acquisition and during the latter half of 2007 announced agreements to acquire CRI Advantage, Inc., an information technology consulting firm, WOW Global Corporation, an information technology consulting and staff augmentation company and CaminoSoft, Inc. a software and services company. These acquisitions are expected to close following the Registrant’s obtaining sufficient funds through a financing to consummate the transactions.

The Information Intellect subsidiary had developed, marketed and licensed a line of enterprise asset management software solutions to companies in the utility industry. On August 17, 2007, Information Intellect and Riptide sold its Acufile and IntelliPlant Software and associated intellectual property rights to PowerPlan Consultants, Inc., for cash proceeds of $1,000,000. Subsequent to the sale, Information Intellect withdrew from the utility industry market and closed its office in Marietta, Georgia. The results of operations of the Information Intellect software business are reflected as discontinued operations in the Riptide financial statements for the years ended December 31, 2007 and 2006....

We have received a report from our independent registered public accounting firm for our year ended December 31, 2007 containing an explanatory paragraph that describes the uncertainty regarding our ability to continue as a going concern. We have experienced recurring operating losses in 2007 and in 2006, have a working capital deficit of approximately $10.5 million, are in default on various debt agreements and total liabilities exceed total assets. Uh oh. That is who wanted to buy SCO's assets?

It goes on and on, of course. One of their products is Resort Management System for "hospitality industry", and they call it, funnily enough, RMS. But don't let that fool you. They are mostly proprietary folks, though they'll use Open Source if it suits: Under a project for a large resort company Riptide Software developed an application that included a full Java 2 Enterprise Edition (J2EE) application using a Microsoft Windows-based GUI (using Java Swing components), an Oracle Database and an IBM MQ Series interface to legacy systems....

The EPS was developed using the latest Microsoft ASP.NET web technologies and leverages the open source DotNetNuke framework. The portal has an intricate role based security model, where members of the portal are given appropriate roles according to their security level and need. Furthermore, every page and module on a page is permission based and can be configured easily to only be viewed by certain roles. There is a SQL Server 2005 backend database that is used to store all data. Custom module development is developed using the C#.NET 2.0 programming language. The EPS provides rich portal functionality and also provides a robust platform that can be easily expanded and enhanced. Open source, DotNetNuke components integrate easily into the EPS and complex, custom functionality can be developed using standard development tools....

Riptide Software also provides comprehensive information technology services to organizations of all sizes. Riptide Software is both a Sun Microsystems and a Microsoft Certified Partner and has expertise in all aspects of information technology including networking and security, server administration, enterprise architecture and custom software development. Riptide Software offers everything from small project consulting to recruiting to full information technology outsourcing. So there's the Unix tie in, I suppose, if any of this is actually business.

Under the header "Results of Operations", we note a detail that interests me: On January 2, 2008, we changed our corporate name to Riptide Worldwide, Inc. (“Riptide”) from Shea Development Corp. References to Shea Development Corp. prior to January 2, 2008 have been revised to refer to the Riptide name.

On March 2, 2007, Riptide, a public shell, and Information Intellect, Inc. (“Information Intellect”), a Georgia based hardware and software developer merged in a transaction accounted for as a reverse merger whereby Information Intellect was deemed the accounting acquirer and therefore, the historical financial statements of Information Intellect became the historical financial statements of Riptide following the merger. Information Intellect operated two business units. Each of the businesses were operated and accounted for separately. The first business was a line of legacy asset management software products and implementation services whereby the business unit licensed its software solutions and provided implementation services to companies operating in the utility industry. On August 17, 2007, we sold the intellectual property rights and exited the legacy asset management software business. The results of operations of the legacy asset management software business have been excluded from the results of continuing operations and are presented as discontinued operations in all periods presented.... Impairment Charge

On September 29, 2007, the former Bravera shareholder resigned his position as an officer of the Company effective October 29, 2007. In addition, it was determined that at September 30, 2007 the cash flow expectations of the RBS business had changed requiring us to significantly lower future cash flow expectations from the RBS operations. We subsequently reduced the workforce and operating expense to a level that supported the existing scanning services contracts. We entered into negotiations with the Bravera shareholder to restructure the original terms of the merger agreement and to reduce the consideration paid or payable pursuant to the merger agreement. However, at December 31, 2007 the negotiations had not been successful and legal actions were initiated and are ongoing. As a result of these factors, we determined that the goodwill and other intangible assets recorded at the acquisition date of RBS had been impaired and we recorded an impairment charge to operations of $4,781,888. Due to slow demand for the ETG products and services and our actions to reduce the workforce and operations, we determined that there were not sufficient future cash flows to support the value associated with the unamortized balance of ETG’s intangible assets and the net book value of the property and equipment resulting in an impairment charge to operations of $1,516,354.

Interest Expense

Interest expense increased from $109,086 in 2006 to $1,312,912 in 2007. The increase was related to new borrowing including the Senior Notes and the Seller Notes. Non-cash interest in 2007 was $596,405, of which $560,095 related to the amortization of the discount on the Senior Notes.

Registration Rights Penalty

The Company recognized a penalty of $829,000 at December 31, 2007 for not maintaining the Leverage and Fixed Charge Coverage Ratios required under the Senior Notes and for failure to meet the requirements of the Registration Rights Agreements.

So, this is September of 2007, a month before we find them showing up trying to buy SCO assets. With what, I can't help but wonder?

Maybe like this?We expect that we will acquire companies and businesses that may increase cash flow from operations however no assurances can be made that we will be successful in increasing cash flow from operations following such acquisitions. They thought SCO's legacy products would bring them cash flow?

The Legal Proceedings section is interesting too. Here's a small taste of just one issue: Upon the acquisition of RTWW Business Services, Inc., formerly Bravera, Inc. (“RBS”), on July 16, 2007, the Company’s subsidiary, RBS, assumed the responsibility to negotiate a contingent liability related to a demand letter from the Defense Finance and Accounting Service (“DFAS”) seeking a refund of approximately $747,000 for alleged “overpayments” on a US Navy contract performed by RBS during the years ended December 31, 2006 and 2005. RBS’s prior legal counsel responded to that demand letter, citing the fact that all of the work on that contract was ordered, approved, and accepted for by the US Navy project and contract managers. DFAS did not respond to inquiries made by RBS’s prior legal counsel and RBS then sought a preliminary injunction against any collection activity with the United States District Court in Alexandria, Virginia in a case styled Bravera, Inc. v. U.S. Dept. of Defense, Case No. 1:07 cv 234 (U.S. Dist. Ct., E.D.Va., 2007). That District Court denied the injunction on jurisdictional grounds. RBS appealed the case before the United States Court of Appeals for the Fourth Circuit, in a case styled Bravera, Inc. v. U.S. Dept. of Defense, Case No. 07-1258 (4th Cir. Ct., 2007), where it was still pending as of March 31, 2008. It is the DFAS’s contention that although government officials did order and accept all of the RBS’s work on the subject contract, some of those officials were not authorized to bind the government contractually. In November 2007, RBS received a payment demand letter from the US Treasury Department for approximately $1,000,000 representing the alleged overpayment amount of approximately $747,000 plus accrued interest. RBS’s legal counsel filed a request with the US Treasury to defer collection activities until the dispute between RBS and DFAS could be settled. In addition to the demanded refund, RBS had an outstanding invoice in the amount of $444,935 for customer support services performed under the US Navy contract for which the invoice has been recorded and fully reserved due to the uncertainty of payment from DFAS for the work performed. RBS is in continuing negotiations with the government to resolve the dispute. A liability of approximately $1,000,000 has been recorded at December 31, 2007 representing the amounts in the US Treasury Department demand letter, however because the final outcome of the settlement is subject to ongoing negotiations a final settlement liability cannot be determined.

Here are the members of the board:

| Name |

Age |

Position with Company |

Director Since |

Term Expires |

| Francis E. Wilde |

56 |

Chairman of the Board and Chief Executive Officer |

3/2/2007 |

3/2/2008 |

| Tom E. Wheeler |

47 |

Vice Chairman and EVP, Mergers and Acquisitions |

3/12/2007 |

3/12/2008 |

| Robert C. Pearson |

72 |

Director |

3/12/2007 |

3/12/2008 |

| Alok Mohan |

58 |

Director |

3/12/2007 |

3/12/2008 |

| Philip Loeffel |

39 |

Director and President |

3/12/2007 |

3/12/2008 |

Francis E. Wilde serves as Chairman and Chief Executive Officer. Prior to joining Riptide, Mr. Wilde served as a consultant to public and private companies. Mr. Wilde served as Chief Executive Officer of Tarantella, Inc. from December 2003 until its sale in July 2005 and served as Chairman of the Board of Digital Stream USA, Inc. from February 2002 until October 2003. Mr. Wilde served as President and CEO of Ravisent Technologies, Inc. from August 1997 until August 2001 and was also a Director of Ravisent Technologies, Inc. from August 1997 until January 2002. Mr. Wilde has held executive management positions at IBM, Dell Computer, Memorex Telex, Summagraphics and Academic Systems.

Tom E. Wheeler serves as Vice Chairman and Executive Vice President, Mergers and Acquisition of Riptide. Mr. Wheeler was a founder of Information Intellect and served as its Chief Executive Officer since it spin-out from EDS in 1997 until March 2007. Prior to founding Information Intellect Mr. Wheeler was a Division Vice President for EDS in the Financial Systems Practice for the Utilities Business Unit.

Robert C. Pearson serves as a director of Riptide. Mr. Pearson has been the Senior Vice President of Investments for Renaissance Capital Group, Inc., an investment fund management firm, since April 1997. From May 1994 to May 1997, Mr. Pearson was an independent financial and management consultant primarily engaged by Renaissance. From May 1990 to May 1994, he served as Chief Financial Officer and Executive Vice President of Thomas Group, Inc., a management consulting firm. Prior to 1990, Mr. Pearson spent 25 years at Texas Instruments, Inc. where he served in several positions including Vice President — Controller and later as Vice President — Finance. Mr. Pearson currently is a director of eOriginal, Inc., Aura Sound, CaminoSoft, and Simtek Corporation where he serves as Chairman.

Alok Mohan serves as a Director of Riptide. Mr. Mohan has served as a director of Rainmaker Systems, Inc. since 1996, and as Chairman of the Board since July 2003. Mr. Mohan has also served on the board of directors of Saama Technologies, a privately held technology services firm, since April 2006 and on the board of directors of Tech Team Global, Inc., a provider of outsourced, multilingual help desk services and specialized IT solutions listed on the Nasdaq Global Market, since May 2006. Mr. Mohan served as the Chairman of the board of directors of Tarantella, until its acquisition by Sun Microsystems in 2005. Prior to that appointment, he served in various executive management positions including Santa Cruz Operations also known as SCO, and at NCR. Mr. Mohan also serves on the board of directors of Stampede and Crystal Graphics.

Philip Loeffel serves as a director and in the role of President of Riptide. He previously held the position of Chief Development Officer from July 16, 2007 until his promotion to President on October 25, 2007. Mr. Loeffel was a Co-Founder of Riptide Software, Inc. a wholly owned subsidiary of Riptide, and served as its Chief Executive Officer from December 1999 until its acquisition by Riptide on July 16, 2007. Riptide Software is a custom software programming and information technology services company located in Oviedo, Florida and was acquired by Riptide on July 16, 2007. Prior to founding Riptide Software, Mr. Loeffel held key information technology positions with Software Technology Inc. and Harris Corporation in the Government Aerospace Systems Division. Mr. Loeffel holds a Master of Science in Computer Science and Software Engineering and a Bachelor of Science in Computer Engineering from Florida Institute of Technology. The executive officers are Wilde, Wheeler, Loeffel, and Richard Connelly as CFO and E. Joseph Vitetta, Jr. as Executive Vice President and Secretary. So, that is Riptide, formerly known as Shea: Richard Connelly assumed his duties on April 2, 2007, as Senior Vice President and Chief Financial Officer of Riptide and its subsidiaries. From March 2002 until March 2007, Mr. Connelly served as Chief Financial Officer of Citadel Security Software, Inc., a security software company and CT Holdings Enterprises, Inc., a technology business incubator. Prior to March 2002 Mr. Connelly served as Chief Financial Officer for several venture funded technology enterprises including, ASSET InterTech, Inc., JusticeLink, Inc. and AnswerSoft, Inc. and performed in various financial management capacities at Sterling Software Inc., Photomatrix Corporation and Texas Instruments, Inc. Mr. Connelly began his career in public accounting, holds a Bachelors of Science in Accountancy from the University of Illinois, a Masters in Finance from the University of Texas at Dallas and is a Certified Public Accountant in the State of Texas.

E. Joseph Vitetta, Jr. serves Riptide as Executive Vice President Corporate Development and Secretary. Mr. Vitetta has previously served as a consultant to both public and private companies. Mr. Vitetta served as Vice President, Corporate Development and Secretary of Tarantella, Inc. from December in December 2003 and served as Executive Vice President, Corporate Development at Starlight Digital Technologies, LLC from February 2003 until December 2003. While at Axeda Systems, Inc. (formerly known as Ravisent Technologies, Inc. and Quadrant International), Mr. Vitetta served as Vice President, Corporate Development from September 1998 until February 2003. So, if I've understood it, Vitetta joined Tarantella in December of 2003, after the SCO saga began. SCO sued IBM in March of 2003. The bio doesn't say what he did after Tarantella was bought by Sun in July of 2005 until he joined Information Intellect, Inc., a wholly owned subsidiary of Riptide, on March 2, 2007. Mohan "receives $7,500 per month for consulting with the Company" as well, and here's why, from the labyrinthian section titled "Item 12. Certain Relationships and Related Transactions, and Director Independence":In 2007, the Company entered into a software development agreement with Saama Technologies, Inc. (“Saama”), a company that participated in the March 2007, Series A Stock transaction. Approximately $1,362,973 was charged by Saama for software development services during the year ended December 31, 2007. At December 31, 2007 a liability to Saama of approximately $952,000 is recorded. In addition, a member of the Company’s board of directors, Mr. Alok Mohan has received consulting fees of $82,500 during 2007 from the Company is also a director of Saama. Wilde, Wheeler, Loeffel, Mohan, Connelly, Vitetta are all listed as shareholders, along with Richard Smithline, Renaissance Capital Group, Lewis Asset Management, Bridgepointe Master Fund, Christopher Watson (who is listed as litigating with the company), and Barry Clinger. Tarantella owned Rainmaker stock in 2004, but then it sold it in the third quartet for $0.9 million, which you can read about in this Tarantella Prospectus Supplement dated May 26, 2005, supplementing the

January 11, 2005 prospectus, by which time the company had incurred a net loss in the millions from operations for the first six months of 2005, as well as for 2004 and 2003, and in fact there were "substantial net losses" for the previous five years. In July of 2005, Sun and Tarantella merged. Here's the 14A, and in it we find that in February of 2005, the top brass entered into a change of control agreement, which you can read about in the document in full, but here's what some of the players got:

Amendments to a Change in Control Agreement with Francis E. Wilde. On February 11, 2005, we entered into an amendment to a change in control agreement with Mr. Wilde dated as of March 16, 2004. Pursuant to the amendment, if Mr. Wilde is involuntarily terminated in connection with a change in control, he is entitled to receive a termination payment. Under the terms of the merger agreement, however, all employees with benefits triggered in whole or in part by a change in control will be entitled to such benefits upon the closing regardless of any termination provisions in the agreements. Therefore, if there is a change in control as defined above for an amount equal to or less than $48 million, Mr. Wilde will be entitled to receive a payment equal to 12 times his total monthly compensation including targeted bonuses at 100% attainment. In addition, all stock options granted to Mr. Wilde will vest and become fully exercisable upon the closing of the merger. If that payment constitutes a “parachute payment” within the meaning of Section 280G(b)(2) of the Internal Revenue Code of 1986, as

amended, and would result in all or a portion of the payment being subject to excise tax under the Internal Revenue Code, then Mr. Wilde would receive a lesser payment so that no portion of the payment would be subject to the excise tax. Mr. Wilde and his dependents will also be entitled to continue to be eligible to participate in health benefit plans on the same terms and conditions as in effect prior to the change in control for up to 12 months. Under the amendment, Mr. Wilde will be entitled to receive cash in the amount of $225,000 in addition to an estimated $15,600 for health care. Mr. Wilde holds 475,000 options, of which unvested options to purchase 394,375 shares will accelerate and vest in full at the effective time. None of those options are in-the-money.

Change in Control Agreements with John M. Greeley, Stephen Bannerman and E. Joseph Vitetta, Jr. On February 11, 2005, we entered into amendments to change in control agreements with each of Messrs. Greeley, Bannerman and Vitetta dated as of March 16, 2004. Pursuant to the agreements, if either Mr. Greeley, Mr. Bannerman or Mr. Vitetta, respectively, is involuntarily terminated in connection with a change in control, he is entitled to receive a termination payment. Under the terms of the merger agreement, however, all employees with benefits triggered in whole or in part by a change in control will be entitled to such benefits upon the closing regardless of any termination provisions in the agreements. Therefore, if there is a change in control as defined above for an amount equal to or less than $48 million, each of Messrs. Greeley, Bannerman and Vitetta will be entitled to receive a payment equal to 12 times his total monthly compensation including targeted bonuses at 100% attainment. In addition, all stock options granted to each of Messrs. Greeley, Bannerman and Vitetta will vest and become fully exercisable upon the closing of the merger. If that payment constitutes a “parachute payment” within the meaning of Section 280G(b)(2) of the Internal Revenue Code of 1986, as amended, and would result in all or a portion of the payment being subject to excise tax under the Internal Revenue Code, then each of Messrs. Greeley, Bannerman and Vitetta would receive a lesser payment so that no portion of the payment would be subject to the excise tax. Each of Messrs. Greeley, Bannerman and Vitetta and their dependents will also be entitled to continue to be eligible to participate in health benefit plans on the same terms and conditions as in effect prior to the change in control for up to 12 months. Under their respective agreements, Messrs. Greeley, Bannerman and Vitetta will be entitled to receive cash in the amounts of $300,000, $315,000 and $366,000, respectively, in addition to an estimated $15,600, $16,800, and $16,800, respectively, for health care. Messrs. Greeley, Bannerman and Vitetta hold 347,500, 145,000 and 222,500 options, respectively, of which unvested options to purchase 278,125, 118,500 and 186,250 shares, respectively, will accelerate and vest in full at the effective time. None of those options are in-the-money.

Change in Control Agreement with Alok Mohan. We entered into a change in control agreement with Mr. Mohan dated as of February 11, 2005. Under this agreement, if there is a change in control as defined above for an amount equal to or less than $48 million, Mr. Mohan’s change in control payment will be equal to the aggregate of (i) the target incentive payment contemplated under his 2005 Consulting Agreement on the basis of 100% attainment and (ii) one times the annual compensation contemplated under his 2005 Consulting Agreement in an amount of $90,000 payable in cash, as adjusted to reflect any amounts and stock (based on the original value of the stock on the date of grant) already earned under the 2005 Consulting Agreement to ensure that Mr. Mohan receives a payment equal to two full year’s annual compensation. In addition, all stock options and restricted stock granted to Mr. Mohan will vest and become fully exercisable immediately prior to the change in control. Under his change in control agreement, Mr. Mohan will receive approximately $150,000 in cash although the actual amount of cash compensation that Mr. Mohan will receive will depend on the amount of unearned restricted stock under his Consulting Agreement that was accelerated at the effective time. The value of this accelerated, unearned restricted stock (based on the original value of the stock on the date of grant) is deducted from the cash payable for the annual compensation component of $90,000. Mr. Mohan will also receive an estimated $20,400 for health care. Mr. Mohan holds 373,603 options and 75,658 shares of unvested restricted stock awards of which 16,447 shares relate to deferred director compensation and 59,211 shares relate to deferred consulting compensation. Mr. Mohan’s unvested options to purchase 142,750 shares will accelerate and vest in full at the effective time, of which 21,600 options are in-the-money and may be cashed out at the effective time for $9,720. The unvested restricted stock awards will fully vest as paid-in-full at the effective time and may be cashed out at that time for $68,092.20. Very prescient change of control agreement, I'd say, in the just in the nick of time kind of way. If you had only joined in 2003, I'd say you cleaned up. Tarantella got swallowed by Sun. Riptide did survive, though, and LinkedIn describes them like this: Founded in 1995, Riptide Software, Inc. is a CMMI Level 3 formally assessed small business providing advanced software solutions and services to civilian and military government agencies and commercial customers in multiple industries. For the past 10 years Riptide has provided products and services to the armed forces live training communities. Riptide is the only industry partner to contribute to all PEO STRI Live Training Transformation product line software products, priming four. Utilizing the latest technologies, Riptide has developed state-of-the-art systems for military C3 systems and simulation systems used in Live Training, Virtual Training, and Constructive Training.

Riptide has extensive experience in designing and implementing high volume, mission critical business solutions. Riptide's enterprise software products provide customers with a wide array of options to make the product their own through a unique configuration process. Enterprise-wide installations are extensively tested prior to final integration and deployment with clients’ existing systems to guarantee an efficient transition with minimal downtime and zero defects.

Riptide offers an established and comprehensive infrastructure designed to efficiently deliver mid to large-scale software solutions. Projects are implemented by the experienced staff at Riptide and each project is managed by a qualified team chosen specifically based on their expertise. The hand-picked team is trained in both object oriented and service oriented architecture (SOA) and utilizes the latest Microsoft, Java and J2EE technologies. Riptide is both a Microsoft Certified Partner and a SUN Microsystems Partner.

So that's Riptide and a bit about all the others, all the same people who tried earlier to buy SCO but were blocked by the court. Will they show up at the auction? They have a notice. That's all we know. Hopefully, they won't be the only ones showing up.

Update 4: This has to be the best headline about SCO ever, from TechDirt, Unix For Sale: Massively Damaged, Sold As Is & Absent Delusions Of Grandeur Over Linux Copyright Infringement. Like all great headlines, it's sort of right, in that it isn't exactly UNIX for sale, but that's too complex for a headline, and anyway it definitely feels right. The bids on TechDirt began at $5, and it's up to $5.11. And that feels right too. ♪ Santa Baby, slip some Unix under the tree, for me. ♫ I've been an awful good grrl.♪

|

|

|

|

| Authored by: Anonymous on Friday, September 17 2010 @ 05:29 PM EDT |

| first post lol [ Reply to This | # ]

|

| |

| Authored by: alisonken1 on Friday, September 17 2010 @ 05:37 PM EDT |

Place a quick one in the subject like "kerrecsions -> corrections",

then follow with the rest in the comment.

---

- Ken -

import std_disclaimer.py

Registered Linux user^W^WJohn Doe #296561

Slackin' since 1993

http://www.slackware.com

[ Reply to This | # ]

|

- humungus > humungous/humongous - Authored by: Anonymous on Friday, September 17 2010 @ 05:40 PM EDT

- filling --> filing - Authored by: Anonymous on Friday, September 17 2010 @ 06:23 PM EDT

- plugged nickel -> plug nickel - Authored by: mexaly on Friday, September 17 2010 @ 06:28 PM EDT

- Versata, Inc. - Authored by: SRL on Friday, September 17 2010 @ 10:56 PM EDT

- Versata, Inc. - Authored by: PJ on Saturday, September 18 2010 @ 01:59 AM EDT

- nickle -> nickel - Authored by: Anonymous on Saturday, September 18 2010 @ 05:35 AM EDT

- Updated 2Xs -> Updated 3Xs - Authored by: bugstomper on Saturday, September 18 2010 @ 03:49 PM EDT

- Comments disappearing ?!! - Authored by: Anonymous on Sunday, September 19 2010 @ 06:03 AM EDT

- Taramtella -> Tarantella - Authored by: symbolset on Sunday, September 19 2010 @ 09:57 PM EDT

- third quartet -> third quarter - Authored by: DaveJakeman on Monday, September 20 2010 @ 06:59 AM EDT

- Please confirm: SVP==Senior Vice President - Authored by: Anonymous on Monday, September 20 2010 @ 11:41 AM EDT

- BOLD newspicks again - Authored by: Anonymous on Tuesday, September 21 2010 @ 04:18 AM EDT

| |

| Authored by: alisonken1 on Friday, September 17 2010 @ 05:39 PM EDT |

Remember clickies and "HTML MODE" at the bottom, and don't forget that

newspicks scroll off, so include a link in the comment.

---

- Ken -

import std_disclaimer.py

Registered Linux user^W^WJohn Doe #296561

Slackin' since 1993

http://www.slackware.com

[ Reply to This | # ]

|

- IE9 and XP - Authored by: celtic_hackr on Friday, September 17 2010 @ 08:59 PM EDT

- XP 9 years old - Authored by: MadTom1999 on Saturday, September 18 2010 @ 03:05 AM EDT

- XP 9 years old - Authored by: cr on Wednesday, September 22 2010 @ 04:17 AM EDT

- XP 9 years old - Authored by: Anonymous on Thursday, September 23 2010 @ 05:32 AM EDT

- IE9 and XP: platform evolution - Authored by: Anonymous on Saturday, September 18 2010 @ 05:15 AM EDT

- Nor will it run on Linux. - Authored by: Alan(UK) on Saturday, September 18 2010 @ 06:02 AM EDT

- IE9 and XP - Authored by: Anonymous on Saturday, September 18 2010 @ 09:02 AM EDT

- IE9 and XP - Authored by: Anonymous on Saturday, September 18 2010 @ 09:17 AM EDT

- IE9 and XP - Authored by: Barbie on Saturday, September 18 2010 @ 12:28 PM EDT

- PEBCAK - Authored by: proceng on Sunday, September 19 2010 @ 05:46 AM EDT

- IE9 and XP - Authored by: Anonymous on Sunday, September 19 2010 @ 09:39 AM EDT

- IE9 and XP - Authored by: celtic_hackr on Monday, September 20 2010 @ 11:54 AM EDT

- A few comments... - Authored by: Anonymous on Saturday, September 18 2010 @ 10:00 AM EDT

- IE9 and XP - Authored by: Anonymous on Saturday, September 18 2010 @ 01:08 PM EDT

- IE9 and XP - Authored by: Anonymous on Saturday, September 18 2010 @ 03:49 PM EDT

- In today's economic climate? - Authored by: Anonymous on Saturday, September 18 2010 @ 05:41 PM EDT

- GPU - Authored by: Anonymous on Saturday, September 18 2010 @ 09:07 PM EDT

- GPU - Authored by: Anonymous on Sunday, September 19 2010 @ 05:59 AM EDT

- XP is available until 2014 at least - Authored by: symbolset on Saturday, September 18 2010 @ 02:27 PM EDT

- Firefox and Chrome can - Authored by: Anonymous on Sunday, September 19 2010 @ 11:32 AM EDT

- IE9 and XP - Authored by: tknarr on Sunday, September 19 2010 @ 01:44 PM EDT

- IE9 and XP - Authored by: Wol on Monday, September 20 2010 @ 10:08 AM EDT

- this XP user giggles at this - Authored by: skyisland on Sunday, September 19 2010 @ 06:16 PM EDT

- Can Linux be the tail that wags the dog? - Authored by: Anonymous on Sunday, September 19 2010 @ 06:56 PM EDT

- IE9 and XP - Authored by: Anonymous on Monday, September 20 2010 @ 07:45 AM EDT

- Microsoft takes Oracle side - Authored by: hopbine on Saturday, September 18 2010 @ 12:55 PM EDT

- Novell may be sold off in two parts, newspaper reports - Authored by: Anonymous on Saturday, September 18 2010 @ 01:22 PM EDT

- Oracle, Google, and Microsoft - Authored by: Anonymous on Saturday, September 18 2010 @ 01:50 PM EDT

- Trade Practices Implications of Infringing Copies of Open Source Software - Authored by: tiger99 on Sunday, September 19 2010 @ 06:59 AM EDT

- Mageia - a Mandriva fork - Authored by: Anonymous on Sunday, September 19 2010 @ 07:51 AM EDT

- Senators Urge Reid to Quickly Bring Amended Patent Reform Bill to Vote - Authored by: Anonymous on Sunday, September 19 2010 @ 09:41 AM EDT

- Microsoft: Use Windows or we'll sue you - Authored by: Anonymous on Sunday, September 19 2010 @ 01:15 PM EDT

- Diaspora NEEDS to change that part... or else they will GO NOWHERE AT ALL, period. - Authored by: Anonymous on Monday, September 20 2010 @ 10:41 PM EDT

- Diaspora contributor agreement - Authored by: odysseus on Tuesday, September 21 2010 @ 04:45 AM EDT

- Xerox PARC turns 40: Marking four decades of tech innovations - Authored by: JamesK on Tuesday, September 21 2010 @ 08:30 AM EDT

- Hurd and HP bury the hatchet - Authored by: Anonymous on Tuesday, September 21 2010 @ 12:51 PM EDT

- cyber attack - Authored by: Anonymous on Tuesday, September 21 2010 @ 11:03 PM EDT

- cyber attack - Authored by: Anonymous on Tuesday, September 21 2010 @ 11:04 PM EDT

- Sending Court Docs to wrong address - Authored by: complex_number on Wednesday, September 22 2010 @ 12:08 PM EDT

| |

| Authored by: alisonken1 on Friday, September 17 2010 @ 05:41 PM EDT |

Don't forget clickies, "HTML MODE", and any thing else you can think

of.

On-topic in here subject to unstoppable replays of DmB testimony played as

background music.

---

- Ken -

import std_disclaimer.py

Registered Linux user^W^WJohn Doe #296561

Slackin' since 1993

http://www.slackware.com

[ Reply to This | # ]

|

- Lawsuits over "Who dat" - Authored by: digger53 on Friday, September 17 2010 @ 05:58 PM EDT

- Webster comments: Broderick Tastes the Bait - Authored by: SpaceLifeForm on Saturday, September 18 2010 @ 01:28 AM EDT

- Investment confusion - Authored by: SpaceLifeForm on Saturday, September 18 2010 @ 01:49 AM EDT

- Dilbert - Authored by: Anonymous on Saturday, September 18 2010 @ 05:55 AM EDT

- Dilbert - Authored by: Anonymous on Saturday, September 18 2010 @ 12:28 PM EDT

- Shuttleworth: Why I do what I do - Authored by: Anonymous on Saturday, September 18 2010 @ 10:44 AM EDT

- Mageia – A New Linux Distribution - Authored by: Anonymous on Saturday, September 18 2010 @ 01:04 PM EDT

- Goat waving contest - Authored by: SpaceLifeForm on Saturday, September 18 2010 @ 04:38 PM EDT

- Filmmaker Premieres Movie In Theaters and on The Pirate Bay - Authored by: The Mad Hatter r on Saturday, September 18 2010 @ 06:13 PM EDT

- Personal DVD burning - advice - Authored by: Anonymous on Saturday, September 18 2010 @ 08:10 PM EDT

- 19 September = Talk Like a Pirate Day... Aargh - Authored by: Anonymous on Saturday, September 18 2010 @ 10:23 PM EDT

- Guess who isn't goin to buy any more Intel chips - Authored by: tyche on Saturday, September 18 2010 @ 11:56 PM EDT

- Nigeria Torture Case Decision Exempts Companies From U.S. Alien Tort Law - Authored by: Anonymous on Sunday, September 19 2010 @ 01:52 AM EDT

- Techcrunch Reports that Cuil may be dead - Authored by: The Mad Hatter r on Sunday, September 19 2010 @ 11:18 AM EDT

- Hole in Linux kernel provides root rights - Authored by: Anonymous on Sunday, September 19 2010 @ 01:08 PM EDT

- BSA's Latest Study on Piracy and Economic Benefits "Shockingly Misleading" - Surprised ? - Authored by: Anonymous on Monday, September 20 2010 @ 09:24 AM EDT

- Nasty .net insecurity. - Authored by: UncleVom on Monday, September 20 2010 @ 10:42 AM EDT

- Microsoft: The Real Tipping Point? - Authored by: DaveJakeman on Monday, September 20 2010 @ 11:59 AM EDT

- Media mergers the latest stab at ‘walled garden’ strategy - Authored by: JamesK on Monday, September 20 2010 @ 12:14 PM EDT

- Oracle's OLTP Benchmarks... - Authored by: Anonymous on Monday, September 20 2010 @ 03:57 PM EDT

- Yup, sure needs to sue the world... - Authored by: dfblakle on Monday, September 20 2010 @ 07:13 PM EDT

- Calibre eBook software Groklaw news recipe - Authored by: Anonymous on Monday, September 20 2010 @ 10:15 PM EDT

- Update: Viacom’s $1 billion copyright lawsuit against YouTube. - Authored by: Gringo on Monday, September 20 2010 @ 10:46 PM EDT

- oracle not so innovative? - Authored by: designerfx on Tuesday, September 21 2010 @ 11:20 AM EDT

- King County [WA] Library System goes Open Source - Authored by: Anonymous on Tuesday, September 21 2010 @ 01:04 PM EDT

- MPAA Wants To Know If ACTA Can Be Used To Block Wikileaks? - Authored by: SpaceLifeForm on Tuesday, September 21 2010 @ 08:09 PM EDT

- Jury Vindicates Former Linspire Employees of 3-Years of Attacks by Michael Robertson! - Authored by: The Mad Hatter r on Tuesday, September 21 2010 @ 10:09 PM EDT

- Terry Pratchett Made His Own Meteorite-Powered Sword After He Was Knighted - Authored by: The Mad Hatter r on Tuesday, September 21 2010 @ 10:12 PM EDT

- Are “Super Angels” in Collusion and Price Fixing ? - Authored by: Anonymous on Tuesday, September 21 2010 @ 11:10 PM EDT

- Mozilla joins OIN - Authored by: Anonymous on Wednesday, September 22 2010 @ 12:52 AM EDT

- Useful BBC Web column - Authored by: RPN on Wednesday, September 22 2010 @ 06:04 AM EDT

- CHANGE - obamanaitor - Authored by: Anonymous on Wednesday, September 22 2010 @ 08:21 AM EDT

- Old but interesting, and it involves SCO! - Authored by: tiger99 on Wednesday, September 22 2010 @ 11:18 AM EDT

- Vulnerability in ASP.NET - Authored by: Anonymous on Wednesday, September 22 2010 @ 12:43 PM EDT

- Veracode (who?) says half of cloud apps have security problems - Authored by: Anonymous on Wednesday, September 22 2010 @ 01:18 PM EDT

- “Danger, Will Robinson!” - HTML5 and evercookie - Authored by: SpaceLifeForm on Wednesday, September 22 2010 @ 01:57 PM EDT

| |

| Authored by: alisonken1 on Friday, September 17 2010 @ 05:44 PM EDT |

If you helped with transcribing COMES documents, place them here for PJ

---

- Ken -

import std_disclaimer.py

Registered Linux user^W^WJohn Doe #296561

Slackin' since 1993

http://www.slackware.com

[ Reply to This | # ]

|

| |

| Authored by: Anonymous on Friday, September 17 2010 @ 07:47 PM EDT |

Some how this vaguely reminds me of the final episode of a sitcom (e.g.

Seinfeld), where anyone who has been on the show reappears.

[ Reply to This | # ]

|

| |

| Authored by: The Mad Hatter r on Friday, September 17 2010 @ 07:59 PM EDT |

Especially the last page. It really makes you wonder what is going on.

---

Wayne

http://madhatter.ca/[ Reply to This | # ]

|

| |

| Authored by: benw on Friday, September 17 2010 @ 08:15 PM EDT |

That's the one thing that really leaps out at me.

Another question is ... why *isn't* there a creditors' committee of some sort,

simply by virtue of how many creditors there are?[ Reply to This | # ]

|

| |

| Authored by: Anonymous on Friday, September 17 2010 @ 10:01 PM EDT |

If they printed single sided, they can turn the paper over and use it as a

notepad. [ Reply to This | # ]

|

| |

| Authored by: Anonymous on Friday, September 17 2010 @ 10:03 PM EDT |

If so I have two thoughts:

1. Here these poor folks are now forever associated with SCO.

2. One of the only valuable assets is now available for free.[ Reply to This | # ]

|

- Nevermind... - Authored by: Anonymous on Friday, September 17 2010 @ 10:07 PM EDT

| |

| Authored by: Anonymous on Friday, September 17 2010 @ 10:31 PM EDT |

Lets say you get paid for negotiating a sale deal. You get paid for work done

not just a percentage of the sale. You are not going to get paid if there are no

parties interested in a sale. But if some party appears from somewhere and says

"I might be interested, tell me more" then you are going to get paid

for collecting information and telling more to the potential buyer. The longer

the potential buyer can stay around without buying anything the longer you get

paid for hourly work as a customer relations operator.

If you work as a sales broker like this. It pays to have a number of friends who

can express buyer interest without having to commit all the way into buying.

Also if you are going to get a part of the final sale then having a bidder who

can fold at the right time but stay in long enough to push up the price helps.

I am not saying this is happening. Just that there are many ways to work the

system.

[ Reply to This | # ]

|

| |

| Authored by: Anonymous on Friday, September 17 2010 @ 11:14 PM EDT |

I suspect that a lot of the names on the list are registered stockholders (e.g.

Alan Petrofsky)

I also noticed that the cost of a share of SCO was down to 6 cents today.

If the first premise is true, they probably spent the equivalent of 100 or more

shares per person.

BTW, the market cap is $1.3M. Should be more like $1.30.[ Reply to This | # ]

|

| |

| Authored by: Anonymous on Saturday, September 18 2010 @ 12:22 AM EDT |

If SCO - which already sold its portable business - is going to sell its UNIX

business, then it has nothing for a business and nothing for a plan to go off

Chapter 11 bankruptcy.

Why NOT just go into Chapter 7, Judge KNCKLHD?[ Reply to This | # ]

|

| |

| Authored by: Anonymous on Saturday, September 18 2010 @ 01:13 AM EDT |

Can Novell go to the auction and bid and pay with the money that SCO

"owes" them? It would be a fitting end to SCO.[ Reply to This | # ]

|

| |

| Authored by: sproggit on Saturday, September 18 2010 @ 04:31 AM EDT |

Some interesting theorising and speculation underway here already, but I wonder

if we could put this into context first?

"The SCO Group" have just lost the "Copyright Trial" with

Novell and now they have put a part of the business up for sale. This brings

forth a series of silly questions:

1. What, precisely, is up for sale? Where's the "Term Sheet", or

whatever the correct legal term is for the document that lists the components

that the seller is offering to sell the buyer?

2. Has The SCO Group actually produced anything to show precisely what they own

[that is not going to be immediately disputed by Novell and/or others]? Granted,

we know that TSG will own all the modifications to the Unixware Product that

they have made since they took over development, but that leaves a huge swath of

the underlying kernel that they did not develop. The Court just found that

Novell owns those underlying copyrights. Are Novell under any obligation to

allow a buyer to continue to sell a "merged product"? Remember, the

buyer cannot sell something they do not own or have not licensed - at least not

without Novell's position, as best as I see it...

3. What's the point of selling now? Given that TSG have indeed filed an appeal,

is the only reason that they are contemplating a sale now is because the

"Pipe Fairy" squad have refused to pony up and more of their own cash,

but want to continue the litigation strategy until it is absolutely stone cold

dead? Whilst this would explain the sale motion, it also suggests - *if* it is

true - that Judge Cahn is "going along with this" strategy, when

perhaps now the best thing to do might be to pay the creditors.

4. Whatever happened to the requirement to file a "Reorganization

Plan"? I seem to remember that when we were still in the "DiP" -

Debtors in Possession stage, i.e. when Darl McBride was still running TSG on a

daily basis, Judge Kevin Gross asked several times for the Management Team to

file a reorganization plan. That request seemed to get a little

"slack" when Judge Cahn became Trustee, because of course he would

need time to get up to speed with the operation of the business. Cahn sought and

Gross approved that Cahn could ask his own legal firm to provide resource to

help him perform that task.

So the way I see it, Cahn has been paid to produce a reorgnization plan that

we're still waiting for, and here he is with another new tactical proposal (no

strategy yet visible) and this one is to sell substantially the remaining

revenue-generating parts of the business. Hmm?

5. What's left if this goes through? Presumably there will be nothing more than

a litigating corpse? Something that ensures that Novell never gets their money? [ Reply to This | # ]

|

- Putting This In Context - Authored by: Wol on Saturday, September 18 2010 @ 08:37 AM EDT

- Reorganization Plan Requirement - Authored by: Jim Olsen on Saturday, September 18 2010 @ 09:41 AM EDT

- SCO's "restructuring plan" - Authored by: Gringo on Saturday, September 18 2010 @ 10:33 AM EDT

- What, precisely, is up for sale? - Authored by: The Mad Hatter r on Saturday, September 18 2010 @ 12:48 PM EDT

- Putting This In Context - Authored by: xtifr on Saturday, September 18 2010 @ 02:44 PM EDT

- Lawsuit lottery was ordered pursued. - Authored by: Anonymous on Saturday, September 18 2010 @ 02:53 PM EDT

- Its all mud - Authored by: Anonymous on Saturday, September 18 2010 @ 03:15 PM EDT

- what does the context say about any buyer? - Authored by: mcinsand on Monday, September 20 2010 @ 08:05 AM EDT

| |

| Authored by: Anonymous on Saturday, September 18 2010 @ 12:58 PM EDT |

Aside from the fact that it appears they want to auction off a bunch of what is

still Novell's property, another question comes to mind.

What about the Yarrow loan - where Ralph gets all the assets of SCO in the event

of a loan default? If SCO auctions off pretty much everything (with the

exception of the litigation stuff which is a worthless money pit to begin with),

there won't be anything left for Ralph when that loan is defaulted. I'm sure

part of that loan was made with the understanding that any active SCO Support

agreements which are left (if there are any) might be worth at least $5.00.

However I'm sure any such support agreements are part of this auction.

Of course that is likely part of the plan - ensure there is nothing left to pay

anyone, and nothing of any value at all.[ Reply to This | # ]

|

| |

| Authored by: Anonymous on Saturday, September 18 2010 @ 03:56 PM EDT |

| LSC Holdings LLC of Dayton, Ohio has been hanging around SCO for more than a

year. It presented a last minute DIP loan proposal to Darl McBride in June

2009, undercutting the Stephen Norris "Potemkin" bid. McBride testified that the

DIP loan was for 5 or 6 million, and was presented by a high dollar lawyer from

Proskauer and Rose, Peter Antosyk.

LSC Holdings LLC submitted a business

registration to the Ohio Secretary of State on November 3, 2009. Virtually no

information accompanies the filing except that LSC used a Dayton, Ohio based

paralegal from the lawfirm Dinsmore and Shouhl LLC to do the paperwork.

Dayton Ohio is the former corporate headquarters of NCR, where former SCO

CEO (94-98) Alok Mohan was a SVP. Mohan serves or served as director of a

number of other software companies (Chairman at Rainmaker, Techteam, Saama). NCR

has used the Dinsmore lawfirm in legal appeals. Mohan lists a Dayton Ohio

address on the Certificate of Service list.

Alok Mohan appears on the cert

of service database indicating he retains a financial or equity stake in SCO. A

number of other Dayton, Ohio addresses appear on the cert listing, so his

relationship is not geographically unique.

The 5-6 Million DIP loan, and

the reappearance of LSC as an entity in November 2009 are coordinate with the

expectation that the LSC principals are equity owners who wanted the legal

lottery to move forward, much as the Ralph Yarro DIP loan was meant to heave the

dying SCO over the trial hurdle.

I think the LSC Holdings LLC party

represents an equity holder interested in the "lottery" and someone with an

understanding of the Unix business, and someone who is in competition with the

Yarro. Mohan fits the profile to a tee, but this remains entirely speculative.

The 2007-9 era buyers appear to have equity interests: York, Yarro, perhaps

Mohan, and Wilde. The situation has changed: the lottery chances have been

greatly diminished, Yarro has a superceding priority for 2 Million. Would Mohan

pay Yarro his Two Million just to keep a place holder (stale equity shares) in

the now vanishing lottery? I doubt it, and that means Cahn must find an entirely

new group of potential purchasers. [ Reply to This | # ]

|

| |

| Authored by: Anonymous on Saturday, September 18 2010 @ 06:00 PM EDT |

"Unix For Sale: Massively Damaged, Sold As Is & Absent Delusions Of Grandeur

Over Linux Copyright Infringement"

Clicky[ Reply to This | # ]

|

| |

| Authored by: sysprog on Saturday, September 18 2010 @ 07:46 PM EDT |

Maybe it's due to being a programmer (for almost my whole life), but I frown now

when I see legal bits that are less than precise. Ms. Haidopoulos states in her

deposition, that

3. All envelopes utilized in the service of the

foregoing contained the following legend:

"LEGAL DOCUMENTS ENCLOSED. PLEASE

DIRECT TO ATTENTION OF ADDRESSEE,

PRESIDENT OR LEGAL

DEPARTMENT."

Unless this is falls under a "term of art" argument,

she is

imprecisely incorrect. The "legend" that she refers to is printed on the

first (facing) page that's inserted into the envelope, and the envelope has a

very large window on its face. However, depending on how the envelope is shaken

(and, perhaps depending on how any given pack of enclosed papers were folded, or

the envelope actually sealed), the part that shows through the window could be

as little as

Legal Documents

Please direct to th

of the

Addressee,

Legal Departmen

[ Reply to This | # ]

|

| |

| Authored by: gstovall on Saturday, September 18 2010 @ 09:17 PM EDT |

Interesting analogy, PJ, comparing these various firms to family relations here

in the Ozarks.

However, the "creepily" part is a bit out of line, at least in

relation to the Ozarks. I live here in the Ozarks (moved here about 7 years

ago), and while I'm not related to the people here, it's true that family

relations are quite widespread. But it's not creepy. It's pretty normal for a

population that is small and rural and happy to remain where they are. While

nearly everyone here is quite low on the income scale, most live a good quality

life with deeply satisfying social interactions with their friends, neighbors,

and family.

I really envy my neighbors at times. While I"m working long hours on yet

another software project, they're out hunting, fishing, spending time with their

children, friends, and family. Who really ends up having the better life?

I spent the 23 years before moving here living in Dallas, so I am well

acquainted with the attractions of a big city. It has come to really disturb me

when I hear urban dwellers being so dismissive of people who have chosen to

remain in the country, as if they are some ignorant hicks that are just too

stupid or lazy to get in the car and move to the city. Now THAT'S creepy! :)[ Reply to This | # ]

|

- Ozarks? - Authored by: Gringo on Saturday, September 18 2010 @ 10:19 PM EDT

- Ozarks? - Authored by: PJ on Sunday, September 19 2010 @ 01:16 AM EDT

- Ozarks? - Authored by: gstovall on Sunday, September 19 2010 @ 09:08 PM EDT

- Ozarks? - Authored by: PJ on Sunday, September 19 2010 @ 09:41 PM EDT

- My Ozark stories - Authored by: Anonymous on Saturday, September 18 2010 @ 11:38 PM EDT

- Dallas? - Authored by: FreeChief on Sunday, September 19 2010 @ 01:53 PM EDT

- Ozarks? - Authored by: benw on Sunday, September 19 2010 @ 02:24 PM EDT

| |

| Authored by: Anonymous on Sunday, September 19 2010 @ 04:44 AM EDT |

♪ Santa Baby, slip some Unix under the tree, for me. ♫

I've been an awful good grrl.♪

Santa Cruz? ;-)[ Reply to This | # ]

|

| |

| Authored by: Anonymous on Sunday, September 19 2010 @ 11:37 AM EDT |

| Let's all chip in and buy it for PJ as a present! [ Reply to This | # ]

|

- No! - Authored by: tiger99 on Sunday, September 19 2010 @ 12:29 PM EDT

| |

| Authored by: Anonymous on Sunday, September 19 2010 @ 07:11 PM EDT |

> I suppose, if any of this is actually business.

[PJ about 5 paras. down on Update 5]

I'd ploughed thru the first quote about "enterprise level solutions ....

"capturing market share in <buzzword> spaces..." so it didn't

surprise me at all to see the second quote marvelling at the cashflow,

drainwards and downwards. People like this have valuable skills in being

able to separate only partly foolish people from their money. The PHBs of

this world exist to supply the desires of the Shea/Riptides.

Their admission that one of their takeover subjects withdrew from its

target market and closed its office rings oh so true. That line was

"enterprise asset management software". As clients we've been thru

three such systems in much the same time scale, for very similar reasons.

Another odd coincidence is that they all used ASP.NET, so maybe

picking up some cheap Unix could give them a better software base.

I doubt it tho', they'd still be chained to IE6, and none of the

systems has actually managed our assets. [ Reply to This | # ]

|

- Riptide. - Authored by: Ian Al on Tuesday, September 21 2010 @ 03:44 AM EDT

| |

| Authored by: symbolset on Sunday, September 19 2010 @ 10:54 PM EDT |

PJ, you seem to have uncovered a hive of villainy related only peripherally

to the SCO debacle. It's an internecine shell game where penny-ante companies

are spawned, merge, are acquired and/or go out of business without ever having

done anything useful. Sometimes they get military or government contracts to do

some things and occasionally deliver, but the prime plot seems to be to strip

investors of their assets on anticipation of impending contracts, and successful

contract bids are accidental. The officers of the companies are board members

of the counterparties and so on, and usually participate in several companies

contiguously. They keep shell companies like most of us keep spare file

folders, and generate more money in legal billings than sales revenues.

It's

a vile practice that could use some light, but I fear it's a rat-hole to drain

your attention down. It's great that you're deep diving the background of these

players in the SCO debacle, but I fear there's no end to these stories that will

ever come to light nor any sense that can be made of it years after the fact.

There are just too many threads to follow. To be fair in the hairball of small

company governance even the players frequently lose the plot in the moment of

action. Double and triple dealing is assumed. They have to be operating at a

higher level of indirection just to stay in this game. Their negotiating

partners are presumed to be playing the same game, and so assumed to be

dishonest on several levels. Each player operates with a desire to build

contingency maps that pay off personally in every case.

This is a game that

asocial genius MBA's play to determine who is the brightest. Score is kept in

dollars and the objective is to get the highest score without doing anything

useful.

There's just not going to be enough provable stuff here to give

returns on your research investment. The whole thing is designed to be

unintelligible. Even if you find some bad action or common thread it won't be

up to your standards of proof to make an allegation - it will just be a fuzzy

thread with commonality of characters who, regardless of their history of

failure continue to make money in positions of responsibility in new

endeavors.

I do however admire your pluck in making the attempt. I went down

this rathole for a few years myself and wound up with nothing more than a list

of people never to do business with. I had to give it up to regain my sanity.

If you pursue this for too long or too far, you're going to be painted with a

tinfoil hat. [ Reply to This | # ]

|

| |

| Authored by: celtic_hackr on Monday, September 20 2010 @ 10:19 AM EDT |

God, my head hurts now.

I need to go take a bottle of Tylenol.

What a mess! PJ needs a Congressional Medal of Honor or something to be able to

put this together. God who could ever figure that out? Maybe that was the point?

How long did it take PJ to sort this all out? And only because of the Bankruptcy

and the open rules thing. And this still only from the fact it went to auction

and notices had to be sent out.

Ugh. I'm so sick of this SCO mess.[ Reply to This | # ]

|

| |

| Authored by: Anonymous on Tuesday, September 21 2010 @ 07:44 AM EDT |

Update 6 talks of the 51% held by common stock. Subsequent actions by the board

give themselves shares etc....

Can anyone guess if the board was trying to counter the 51%? I don't know if it

was a feasible strategy or if the numbers work out that way. Presumably some of

the board members might be among the holders of common stock?

If one was going to take the company in a new direction (to the 'I'm going to

sue you warpath') one might have wanted the ability to stop a common stock

uprising...

Or do the rest of the numbers make this look silly?

s[ Reply to This | # ]

|

| |

| Authored by: mcinsand on Wednesday, September 22 2010 @ 12:18 PM EDT |

Ian_Al confirmed my memory that Novell retained rights to nix any asset sales,

so can Novell warn auction participants that they might no be able to buy what

SCOX is claiming to sell. Moreover, is warning the participants a good step in

Novell publicly maintaining their claims?

Regards,

mc[ Reply to This | # ]

|

|

|

|

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}